Primary the focus; retail engaged as mutual fund inflows continue

Municipals were a touch softer Wednesday, but outperformed U.S. Treasury weakness as investors focused on the primary market with several large new-issues pricing to solid demand. Equities were in the black to close the session.

Triple-A yield curves were little changed to weaker by one to four basis points, depending on the curve, while Treasuries saw larger losses out long.

Muni to UST ratios adjusted downward. The two-year muni-to-Treasury ratio Tuesday was at 63%, the three-year at 63%, the five-year at 64%, the 10-year at 67% and the 30-year at 84%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 63%, the three-year at 64%, the five-year at 64%, the 10-year at 69% and the 30-year at 85% at 4 p.m.

There has been an “incredible” amount of demand for new issues, said Julio Bonilla, a fixed-income portfolio manager at Schroders.

“Even [Wednesday], new issues have cheapened a little bit, but given the violent move in the rates market earlier today, I was a little surprised at how well some of the deals did do,” he said.

Columbia University came to market Wednesday with a $500 million deal: $350 million of taxable corporate CUSIPs through the Trustees of Columbia University and $150 million of revenue bonds from Dormitory Authority of the State of New York.

The university’s deal came at fairly tight spreads, Bonilla said.

The biggest theme within the muni market — and what is responsible for its performance — is the large amount of cash on the sidelines, with $6-plus trillion in money market funds and close to $2.5 trillion in certificates of deposits, he noted.

“That is a lot of liquidity that ultimately has to find a home as rates start to trickle lower at the front end,” he said.

But with each “incremental” cut in the Fed Funds rate, marginal investors will decide to “pull out of the shorter instruments and try to lock in what they can at the long end,” Bonilla said.

An expensive equity market has helped push some of that liquidity over to the muni market, especially when on a tax-adjusted basis, it’s still fairly attractive, he said.

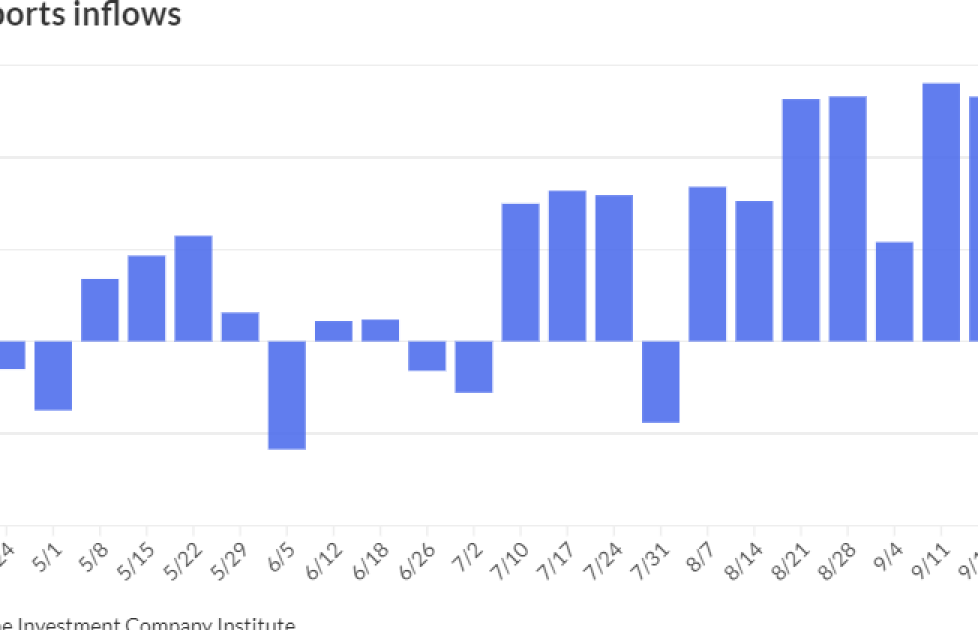

The Investment Company Institute reported $1.312 billion of inflows into municipal bond mutual funds for the week ending Sept. 25 after $1.329 billion of inflows the week prior. Exchange-traded funds saw $109 million of inflows after $55 million of inflows the previous week.

Via ICI data, 2024 year-to-date fund flows have surpassed $20 billion, and separately managed account activity has also remained elevated, “with last week registering 275,000 total trades,” noted Matt Fabian, partner at Municipal Market Analytics, Inc. “However, that the number of trades was down a bit amid much higher volume highlights underwriters’ incremental reliance on fund buying last week.”

“The funds are thus becoming more important for performance, especially as Fed data suggest still flat-at-best bank demand that may be turning more outright negative into quarter end,” Fabian noted.

If the muni market does rally, “hypothetical year-end surge in refundings could put 2024 issuance in reach of a full-year record,” Fabian said. “Demand for all these bonds has been well sustained by retail.”

In the primary market Wednesday, BofA Securities priced for the Kentucky State Property and Buildings Commission (Aa3//AA-/) $600 million of Project No. 131 revenue bonds, with 5s of 10/2025 at 2.70%, 5s of 2029 at 2.53%, 5s of 2034 at 2.89%, 5s of 2039 at 3.23%, 4s of 2044 at 3.87% and 5s of 2044 at 3.59%, callable 10/1/2034.

BofA Securities priced for Massachusetts (Aa1/AAA//AAA/) $489.76 million of Commission Transportation Fund revenue bonds, consisting of $150 million of Rail Enhancement Program bonds, Series 2024A, with 5s of 6/2044 at 3.38%, 5s of 2049 at 3.68% and 5s of 2053 at 3.77%, callable 6/1/2034; $125 million of sustainability Rail Enhancement Program bonds, Series 2024B, wiht 5s of 6/2054 at 3.78%, callable 6/1/2034; and $214.76 million of refunding bonds, Series 2024A, with 5s of 6/2025 at 2.89%, 5s of 2029 at 2.32%, 5s of 2034 at 2.64%, and 5s of 2044 at 3.38%, callable 6/1/2034.

Jefferies priced and repriced for the Northeast Ohio Regional Sewer District (Aa1/AA+//) $163.105 million of wastewater improvement refunding revenue bonds, Series 2024, with 5s of 11/2025 at 2.49%, 5s of 2029 at 2.38%, 5s of 2034 at 2.71% (-3), 5s of 2038 at 2.96% (-1), 5s of 2044 at 3.41%, and 5s of 2046 at 3.53%, callable 11/15/2034.

BofA Securities priced for the Dormitory Authority of the State of New York $150 million of Columbia University revenue bonds, Series 2024A, with 5s of 10/2031 at 2.40% and 5s of 2036 at 2.71%, callable 10/1/2034.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.55% (unch) and 2.28% (unch) in two years. The five-year was at 2.27% (unch), the 10-year at 2.54% (unch) and the 30-year at 3.48% (unch) at 3 p.m.

The ICE AAA yield curve was cut up to four basis points: 2.61% (+4) in 2025 and 2.29% (unch) in 2026. The five-year was at 2.27% (+1), the 10-year was at 2.56% (+1) and the 30-year was at 3.45% (+1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.54% (unch) in 2025 and 2.29% (unch) in 2026. The five-year was at 2.26% (unch), the 10-year was at 2.55% (unch) and the 30-year yield was at 3.45% (unch) at 4 p.m.

Bloomberg BVAL was cut: 2.59% (+5) in 2025 and 2.35% (unch) in 2026. The five-year at 2.31% (unch), the 10-year at 2.57% (unch) and the 30-year at 3.44% (unch) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 3.635% (+1), the three-year was at 3.547% (+2), the five-year at 3.553% (+3), the 10-year at 3.783% (+4), the 20-year at 4.192% (+5) and the 30-year at 4.133% (+5) at the close.

Primary to come:

San Antonio, Texas, (Aa1/AA+/AA/) is set to price Thursday $268.59 million of water system junior lien revenue bonds, Series 2024B. J.P. Morgan.

Competitive:

Alexandria, Virginia, is set to sell $114.92 million of GO capital improvement bonds at 10:30 a.m. eastern Thursday.

Jessica Lerner contributed to this report.