Jobs data snaps rally; investors await smaller calendar, FOMC

Municipals saw losses but outperformed a U.S. Treasury selloff sparked by better-than-expected jobs data while a much smaller primary slate awaits investors ahead of the June Federal Open Market Committee meeting.

The non-farm payrolls data further raises concerns over the timing of the Central Bank’s rate cutting schedule.

“This blockbuster NFP makes it harder for the Fed to move towards a cut in rates,” said Giuseppe Sette, president of Toggle AI. “The next few months will be interesting as the Fed will have to tussle with the stronger performance of the U.S. economy, limiting its ability to follow the example of the [European Central Bank] and cut.”

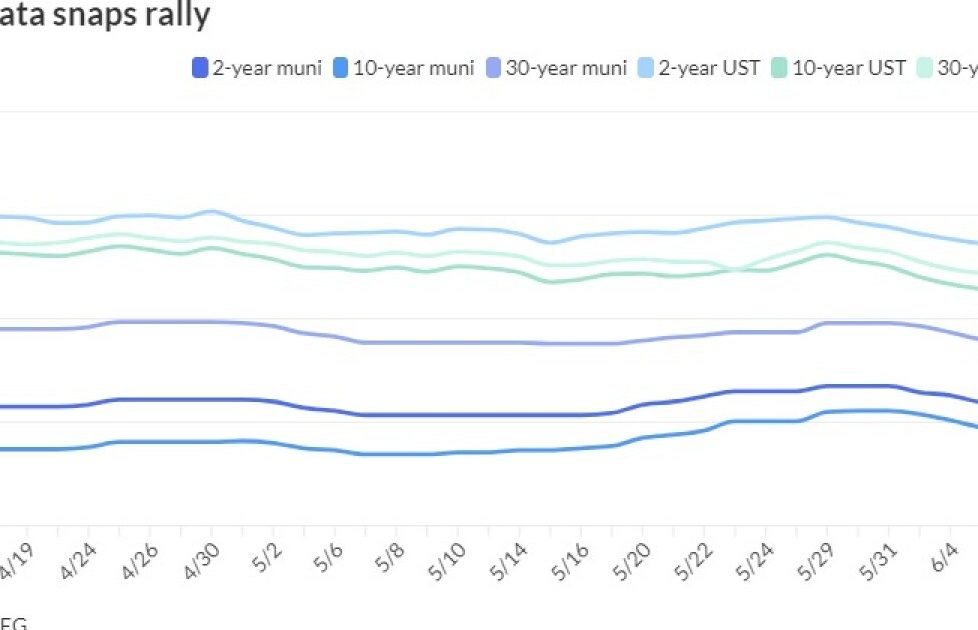

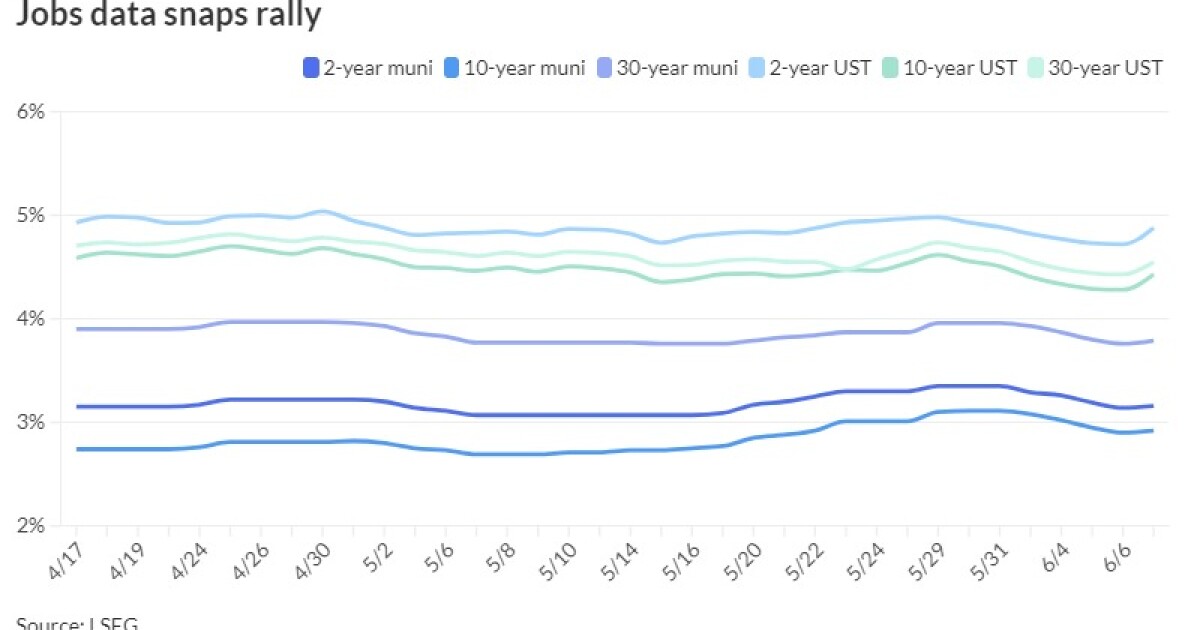

USTs spiked 17 basis points on the short end and 15 to 12 10-years and out following the release, while triple-A curves saw yields rise two to five basis points, depending on the yield curve, in a more muted and typical reaction for the asset class.

The moves came following what had been a rallying market in both munis and USTs all week.

Municipals absorbed a massive, $15 billion-plus new-issue slate while seeing triple-A yields fall by 15 basis points on the two-year, 16 on the five-year, 18 on the 10-year and 17 on the 30-year from Monday to Thursday’s close, according to MMD. Municipal bond

The week’s performance also shows returns as of Friday morning for munis in the black. The Bloomberg Municipal Index is at positive 1.22% month to date, pushing returns in 2024 to -0.71% while the High-Yield Index is at positive 1.46% in June and +3.13% year-to-date. Taxable munis are in the black at +1.67% and +0.53% in 2024 while the Short-Term Index is seeing +0.14% in June and +1.24% year-to-date.

The compares with corporates, showing a +1.18% in June and +0.05% in 2024 and USTs at +1.09% and -3.69% this year.

Ratios, which had risen in May, fell with Friday’s new Treasury levels, pushing muni-to-UST ratios lower again, depending on the triple-A scale.

The two-year muni-to-Treasury ratio Friday was at 65%, the three-year at 65%, the five-year at 67%, the 10-year at 66% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 67%, the three-year at 68%, the five-year at 69%, the 10-year at 69% and the 30-year at 86% at 3:30 p.m.

“In the past two weeks, tax-exempts have quickly given up 8-10 ratios after trading in the 60% area for the first five-plus months of the year — have they become cheap enough or are they just getting close to more-normal levels?” said Barclays PLC strategists in a weekly report. “On the one hand, 68%-70% is still very rich compared with historical levels, even if we account for the current level of rates. Treasury yields were trading at similar levels in 2005-07, but the average for the 10y MMD-UST ratio was 83% over that time period.”

On the other hand, they note, that prior to the 2022-23 rate sell-off, fixed income yields were trading at very low levels for more than a decade, and “investors are finally able to take advantage of relatively reasonable fixed income yields, making them willing participants in fixed income once again, including tax-exempts.”

Next week, the new-issue calendar falls to just over $5 billion, led by Los Angeles County’s $700 million of 2024-2025 tax and revenue anticipation notes, the Massachusetts Water Resources Authority’s $477.255 million of green general revenue bonds and the New York City Housing Development Authority’s $442.025 million of sustainable multi-family housing revenue bonds.

Bond Buyer 30-day visible supply falls to $13.82 billion.

“Even though the muni market feels very good despite the largest supply week in more than a year, we are pretty comfortable asserting that we are definitely not out of the woods,” Barclays PLC strategists Mikhail Foux and Clare Pickering said. “Tax-exempts have performed well this week, but Treasury volatility will likely return … while supply is unlikely to let up any time soon. Thus, we believe investors should not chase this week’s rally, and might be better off lightening up into strength, while waiting for a better entry point down the line.”

AAA scales

Refinitiv MMD’s scale was cut two to three basis points: The one-year was at 3.20% (unch) and 3.16% (+2) in two years. The five-year was at 2.97% (+2), the 10-year at 2.92% (+2) and the 30-year at 3.79% (+3) at 3 p.m.

The ICE AAA yield curve was cut two to five basis points: 3.25% (+2) in 2025 and 3.19% (+3) in 2026. The five-year was at 2.97% (+5), the 10-year was at 2.94% (+5) and the 30-year was at 3.80% (+5) at 4 p.m.

The S&P Global Market Intelligence municipal curve was cut four to five basis points: The one-year was at 3.25% (+2) in 2025 and 3.17% (+2) in 2026. The five-year was at 2.96% (+1), the 10-year was at 2.92% (+1) and the 30-year yield was at 3.77% (+2), at 4 p.m.

Bloomberg BVAL was cut three to five basis points: 3.26% (+2) in 2025 and 3.21% (+2) in 2026. The five-year at 2.98% (+3), the 10-year at 2.92% (+2) and the 30-year at 3.80% (+3) at 4 p.m.

Treasuries sold off.

The two-year UST was yielding 4.885% (+17), the three-year was at 4.665% (+17), the five-year at 4.457% (+17), the 10-year at 4.432% (+15), the 20-year at 4.643% (+13) and the 30-year at 4.55% (+12) at the close.

Jobs data throws cold water on Fed cut expectations

“Payrolls expanding at a monthly average rate of 250k over the last three months does not point to much of a slowdown in labor demand,” noted Brian Coulton, Fitch Rating’s chief economist. “At the same time the household survey tells us that the participation rate and the labor force declined on the month.

“That is not the mix of news on labor supply and demand that the Fed wanted to see in order to corroborate its assessment that labor market imbalances are easing,” Coulton added.

Wells Fargo Investment Institute Senior Global Market Strategist Scott Wren agreed, noting the much stronger-than-expected payrolls in May was “not the report the FOMC wants to see,” adding it wants “weaker employment and wage data.”

Wren said rate cuts are on hold for now, although “clearly few expected cuts in the very near term,” noting Wells anticipates two cuts “penciled in for 2024.”

“We remain more cautious on both equity and fixed income exposure and are looking for better entry points in both asset classes,” Wren said. “We believe there will be opportunities to buy equities at lower valuations and extend duration and buy long-term Treasuries at higher yields.”

John Kerschner, head of U.S. Securitized Products & Portfolio Manager at Janus Henderson Investors, said his firm believes the Fed does want to cut this year, but it’s unlikely to happen until September at the earliest.

“And when they do, it’s likely they message this does not kick off a consistent hiking cycle of 25 bps per meeting, but perhaps a more infrequent cadence such as every other meeting,” Kershner said. “It doesn’t particularly matter if they start hiking in September or in November, what matters is the cadence from there.”

Additionally, an eventual easing cycle “will not normalize the yield curve overnight,” he said.

The deeply inverted U.S. Treasury yield curve “may take quarters, if not years, to right itself.”

“We think this happens with Fed cuts bringing the front end down, while the long end elevated, with room to rise modestly if U.S. inflation remains sticky,” Kerschner said. “It’s important to remember that while investors got comfortable with zero-interest rate policy (ZIRP) over recent years, the 5-year and 10-year at just over 4% aren’t that far off fair value and we expect they can remain at similar levels while the front end of the curve adjusts.

Negotiated calendar

Los Angeles County is set to price Tuesday $700 million of 2024-2025 tax and revenue anticipation notes. Morgan Stanley & Co. LLC

The Massachusetts Water Resources Authority (Aa1/AA+/AA+/) is set to price Tuesday $477.255 million of general revenue bonds, Series B, consisting of $166.265 million of green general revenue bonds, serials 2025-2049, and $310.960 million of green general revenue refunding bonds, serials 2027-2043. Barclays Capital Inc.

The New York City Housing Development (Aa2/AA+//) is set to price Tuesday $442.025 million of multi-family housing revenue bonds, consisting of $134.190 million non-AMT sustainable development bonds, series 1, and $307,835 million of non-AMT sustainable development bonds, series 2. Morgan Stanley & Co. LLC

The Oklahoma Industries Authority (/AA-//) is set to price Tuesday $436.980 million of Oklahoma City Public Schools Project educational facilities lease revenue bonds, series 2024, serial 2025-2034. D.A. Davidson & Co.

The Industrial Development Authority of Mobile County, Alabama, (Baa3/BBB-//) is set to price Tuesday $378 million of AM/NS Calvert LLC Project solid waste disposal revenue bonds, serial 2054. BofA Securities.

The Michigan State University Board of Trustees (Aa2/AA//) is set to sell $363.985 million of general revenue bonds, series 2024A, serial 2025-2044, term 2049, 2054. BofA Securities.

The Maryland Economic Development Corporation (A3///) is set to price Tuesday $345.540 million of

The State of Connecticut Health and Educational Facilities Authority (/AA-/A+/) is set to price Tuesday $322.000 million of Yale New Haven Health Issue revenue refunding bonds, series 2024A and series 2024B, consisting of $160 million serial 2025-2023 and 2044-2048, and $162.000 million, term 2049. Barclays Capital Inc.

The Illinois Finance Authority (Aa3/AA-//) is set to price $284 million of Endeavor Health Credit Group revenue refunding bonds, series 2024A, serial 2030, 2032. BofA Securities.

The Rhode Island Housing and Mortgage Finance Corporation (Aa1/AA+/NR/NR) is set to price Tuesday $194.150 million of homeownership opportunity bonds, consisting of $104 million Series 83-T taxables, $84 million Series 83-A non-AMT social bonds, and $6 million Series 83-B AMT social bonds. J.P. Morgan Securities LLC.

The Chambers County Justice Center Public Facilities Corp., Texas, (/AA-//) is set to price Tuesday $152.950 million of Justice Center Project lease revenue bonds, series 2024. Piper Sandler & Co.

The Minnesota Housing Finance Authority (Aa1/AA+//) is set to price Tuesday $105 million of taxable residential housing finance social bonds, series 2024 M, serial 2025-2036, terms 2039, 2044, 2049, 2051. RBC Capital Markets.

Competitive:

The Johnson County USD #229, Kansas, is set to sell $150 million of general obligation school bonds, Series 2023-A, at noon eastern Monday, and $32.620 million of GO refunding bonds, Series 2023-B at noon eastern Monday.