Munis firmer; market tone continues to be positive

The municipal market tone continues to be positive as munis were firmer again. U.S. Treasury yields fell and equities ended in the black.

Triple-A benchmarks were bumped two to four basis points, depending on the scale, pushing the one-year below 2.50%. UST yields fell three to nine basis points.

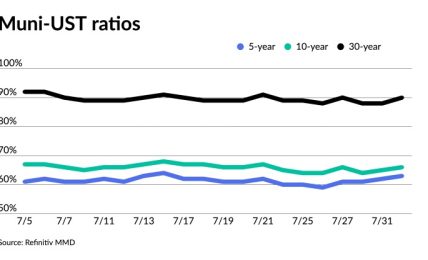

The three-year muni-UST ratio was at 58%, the five-year at 62%, the 10-year at 67% and the 30-year at 90%, according to Refinitiv MMD’s final 3 p.m. ET read. ICE Data Services had the three at 57%, the five at 60%, the 10 at 67% and the 30 at 89% at a 4 p.m. read.

“The municipal market is off to a great start in 2023, which isn’t that surprising considering the significant rise in rates that happened in 2022,” said Roberto Roffo, managing director and portfolio manager at SWBC Investment Services LLC.

“With interest rates at levels not seen for a long time,” Roffo said, “I think investors are focusing on the overall interest rate levels as opposed to rich-cheap ratios.”

The short end of the municipal yield curve offers a good example, he added, as ratios from one year to seven years range from the low 50% range to the mid-60% level and demand remains “very strong” due to absolute interest rate levels, he said.

Investors see a slowing economy that may be headed for recession and still high but moderating inflation levels, Roffo said. These two factors will drive the market for the rest of the year, he believes.

“The common belief is that the Federal Reserve is close to being done raising interest rates and an economic slowdown and lower inflation will fortify that belief, which in turn, will create additional demand for municipal bonds,” Roffo added.

Meanwhile, elsewhere in the buy side market, higher coupons are trending among supply- and yield-hungry investors.

A New York trader on Wednesday said he sees a trend in increasing bids and demand for 5% coupons between eight and 15 years.

Since the spreads on those 5% coupon bonds — rated single and double A — are highly compressed compared to the generic, triple-A yield curve, they are growing in attractiveness, especially amid the overall supply shortage, he said.

“Investors are piling into that portion of the curve,” he said.

The trader said that trend could continue throughout the first quarter — until either rates get cheaper or issuers start bringing deals to market.

“Issuers are not being aggressive in figuring out how to come into the market,” he said.

“It’s been a really interesting start to the year,” said Rick Fogliano, head of municipal products at TD Securities.

“There’s no supply, and we went into last year with no supply,” he said.

“So the ‘January effect’ came in and a lot of people got cash and all of a sudden, people started buying,” Fogliano said. “We’re seeing it across the tax-exempt [space] as well as some of the taxable bonds.”

But unlike 2022, when the world was still reeling from the pandemic, he said, there’s now a sense of stability in munis even though there’s still uncertainty in the market, such as further Federal Reserve rate hikes and the severity of a possible recession.

“The investor and issuer side are both cautiously optimistic about the year and expect things to at least settle at some point where we can get back to some more normalcy, but most do expect some sort of volatility one way or the other in the coming months and the rest of the year,” Fogliano said.

He expects things to go smoother this year than in 2022 where there won’t be “these initial jerky moves.”

Traders continue to sell into strength and pick their spots.

“The story of the year is going to be supply and how it’s going to come in,” he said.

After some good years supply has declined, and Fogliano believes investors will return to a fixed-income product that is more stable and feels safer.

Inflation remains a factor, with Fogliano saying, “it’s hard to buy a fund when you’re not covering the inflation number.” But as inflation comes down, he said, fixed income becomes more interesting and will find buyers.

On the supply-demand dynamic, he said, “the funds that have to be invested —or the alternative is not getting anything — will be invested.”

Investors are cautious about what they buy, with better names trading and high-yield lagging behind the more high-grade names.

Once supply ticks up, which will happen at the end of the month or early February, he said, things will start to normalize.

Munis were very rich, but right now, he said, they’re trying to cheapen a little bit. However, with USTs moving around, munis are “catching a bid, so things have gotten a little tighter” but have cheapened overall.

Last week, munis followed the UST rally, but there was also demand for tax-exempt bonds, said Nuveen strategists Anders S. Persson and John V. Miller.

They expect “this to continue for the next few weeks as the outsized Jan. 1 reinvestment coupon remains to be invested,” while “new issue supply should remain muted during that same period.”

January is a “huge” reinvestment month, Fogliano noted.

“Regardless of whether the market is cheap or rich, there is a lot of cash out there,” he said. “So people are continuing to look to invest.”

When the taxable market sold off in December, he said, muni-UST ratios got “not so great,” but have “come back the other way as things start to grind higher.”

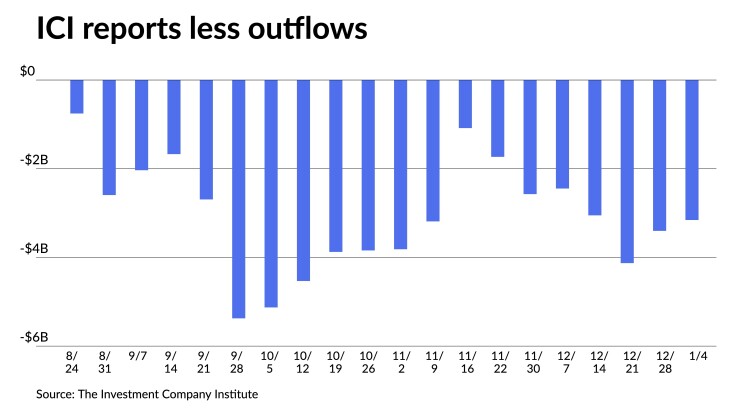

Traditional mutual funds have continued to lose assets. Lipper reported another $3 billion-plus outflow last week: “an atypical start to the new year where risk-on investing usually prevails,” said Matt Fabian, a partner at Municipal Market Analytics.

“Should those fund flows reverse, which appears at least possible following the December jobs report, the tone in tax-exempts could turn unsustainably positive in short order, pushing already low ratios lower still,” he said.

The 10-year muni-UST ratio is at 67%. Despite rising last week due to “the exceptional rally in USTs,” it is still “near the bottom of the range established over the last year.”

“But because this remains a period of mean evolution (versus reversion),” he said, “low ratios are less likely to inhibit demand than in the past; in fact, expected medium-term scarcity in tax-exempt product could underwrite precedentially lower ratios going forward.”

Outflows lessened, with the Investment Company Institute reporting investors pulled $3.157 billion from mutual funds in the week ending Jan. 4, after $3.402 billion of outflows the previous week.

Exchange-traded funds saw inflows of $864 million after $679 million of inflows the week prior, per ICI data.

In the primary market Wednesday, Wells Fargo priced for the Utah Board of Higher Education (Aa1/AA+//) $154.380 million University of Utah green general revenue bonds, Series 2022A, with 5s of 8/2025 at 2.27%, 5s of 2028 at 2.28%, 5s of 2033 at 2.45%, 5s of 2038 at 3.12% and 5s of 2042 at 3.36%, callable 8/1/2032.

In the competitive market, Colorado sold $425 million of Education Loan Program tax and revenue anticipation notes, Series 2022B. The state sold $50 million to BofA Securities with 5s of 2022 at 2.52%.

The state also sold $100 million to Citigroup Global Markets with 5s of 2022 at 2.52%.

Colorado sold $175 million to JPMorgan Securities with 5s of 2022 at 2.52% as well.

Additionally, the state sold $100 million to Morgan Stanley in two deals: $75 million of 4s of 2022 at 2.52% and $25 million of 4s of 2022 at 2.52%.

Secondary trading

New York City 5s of 2024 at 2.42% versus 2.47%-2.43% Tuesday and 2.72% on 1/3. Washington 5s of 2025 at 2.31% versus 2.35% original on Tuesday. Maryland 5s of 2025 at 2.32% versus 2.33% Monday and 2.54% on 1/3.

Gilbert Water Resource Municipal Property Corp., Arizona, 5s of 2030 at 2.28%. Triborough Bridge and Tunnel Authority 5s of 2031 at 2.64% versus 2.94% original on 1/6.

Los Angeles DWP 5s of 2042 at 3.29%-3.28%. NYC TFA 5s of 2043 at 3.60% versus 3.65% Tuesday and 3.90%-3.89% on 1/5.

Massachusetts 5s of 2048 at 3.63%-3.62%. St. Johns County water, Florida, 5s of 2052 at 3.63%. Illinois Finance Authority 5s of 2052 at 4.32%-4.26% versus 4.40% Monday and 4.52%-4.50% on 1/4.

AAA scales

Refinitiv MMD’s scale was bumped two to four basis points: the one-year at 2.48% (-4) and 2.32% (-2) in two years. The five-year was at 2.27% (-2), the 10-year at 2.38% (-3) and the 30-year at 3.31% (-4).

The ICE AAA yield curve was bumped two to four basis points: at 2.46% (-2) in 2024 and 2.34% (-2) in 2025. The five-year was at 2.27% (-3), the 10-year was at 2.38% (-4) and the 30-year yield was at 3.34% (-3) at 4 p.m.

The IHS Markit municipal curve was bumped three basis points: 2.48% (-3) in 2024 and 2.31% (-3) in 2025. The five-year was at 2.29% (-3), the 10-year was at 2.40% (-3) and the 30-year yield was at 3.33% (-3) at a 4 p.m. read.

Bloomberg BVAL was bumped two to four basis points: 2.47% (-4) in 2024 and 2.31% (-4) in 2025. The five-year at 2.27% (-4), the 10-year at 2.38% (-4) and the 30-year at 3.33% (-3).

Treasuries were better.

The two-year UST was yielding 4.218% (-3), the three-year was at 3.915% (-6), the five-year at 3.655% (-6), the seven-year at 3.598% (-7), the 10-year at 3.534% (-8), the 20-year at 3.828% (-8) and the 30-year Treasury was yielding 3.659% (-9) at 4 p.m.

Primary on Tuesday:

RBC Capital Markets priced for the Plano ISD, Texas, (Aaa/AA+//) $631.450 million of unlimited tax school building bonds, with 5s of 2/2024 at 2.53%, 5s of 2028 at 2.36%, 5s of 2033 at 2.49%, 5s of 2038 at 3.15% and 5s of 2043 at 3.44%, callable 8/15/2032.