Munis pressured out long; New deals face concessions

Municipals sold off out long in secondary trading while two billion-dollar-plusnew-issues from California and the New York City Transitional Finance Authority made concessions in primary pricings. Munis continued to play catch up to the rise in U.S. Treasury yields, though taxables improved Wednesday and equities ended mixed.

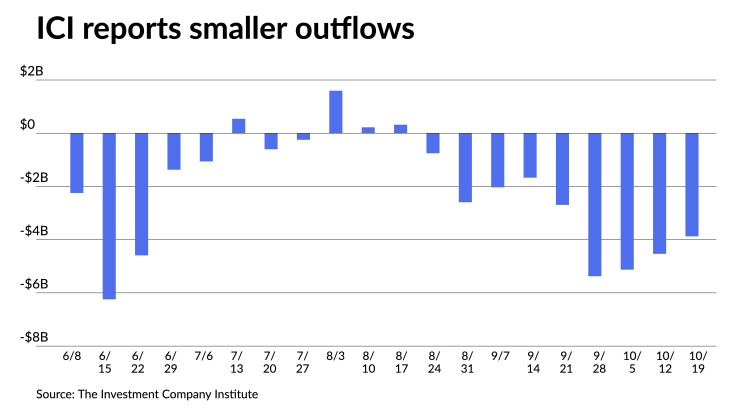

Municipal bond mutual funds saw more losses with the Investment Company Institute reporting another week of multi-billion-dollar outflows, brining year-to-date losses to $115.6 billion.

Investors pulled $3.876 billion from mutual funds in the week ending Oct. 19 after $4.532 billion of outflows the previous week, according to ICI. ETFs saw inflows of $334 million after $2.271 billion of inflows the week prior, per ICI data.

Munis 10-years and in were little changed on the day but the 30-year triple-A yield was cut seven to 20 basis points Wednesday, depending on the scale, while USTs saw yields fall five to nine basis points.

As a result muni to UST ratios rose with the 10-year climbing back up to the mid-80s and the 30-year reaching 100%. The three-year was at 73%, the five-year at 77%, the 10-year at 85% and the 30-year at 100%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the three at 73%, the five at 76%, the 10 at 85% and the 30 at 103% at a 4 p.m. read.

“After a good start to the month, municipals have taken a decidedly negative turn on the back of rising Treasury yields and continuing cash outflows,” Roberto Roffo, managing director and portfolio manager at SWBC Investment Services, LLC, said on Tuesday.

Year-end considerations, rising yields and fund redemptions have combined to create the highest daily bids wanted volume all year, noted Kim Olsan, senior vice president of municipal bond trading at FHN Financial. From Oct. 3 through Tuesday, half of the sessions carried a bid list tally over $2 billion par, per Bloomberg data. Monday’s total was $2.003 billion and Tuesday’s hit $2.265 billion. Lists were elevated again Wednesday.

Olsan said fund outflows are “contributing to the exaggerated [bids wanted] volume as well as an increased line item count.”

“October’s daily items posted for sale have risen 10% as sellers cast a broader net of potential sale candidates,” she said. “Forthcoming fund flow data will confirm whether rising yields are beginning to attract new investors.”

The value of short-dated calls “is collapsing across the coupon stack but notably in 4% coupons with intermediate maturities,” according to Olsan.

Compared to activity in November 2021 at -46/AAA (to yield 0.64%), “California GO 4s due 2031 (callable 2026) recently trading at 3.73% work out to a spread of +40/AAA,” she said.

Short calls, she said, “are widening the spread in intermediate premium 5s as opposed to tightening the bidside as occurred in 2020 and 2021 — when yields sat 200-300 basis points lower.”

Olsan noted “duration has become more in focus with sights set on an eventual easing” of the current Federal Open Market Committee cycle.

In the negotiated market Wednesday, Wells Fargo priced for the New York City Transitional Finance Authority (Aa1/AAA/AAA/) is set to price Wednesday $950 million of tax-exempt future tax secured subordinate bonds, Fiscal 2023 Series D, Subseries D-1, with 5s of 11/2024 at 3.32%, 5s of 2027 at 3.44%, 5s 2037 at 4.41%, 5.25s of 2037 at 4.38%, 5.25s of 2042 at 4.61% and 5.25s of 2048 at 4.80%, callable 11/1/2032.

Wells Fargo priced for the Richardson Independent School District, Texas, (Aaa/AAA//) $193.930 million of unlimited tax school building bonds, Series 2022A, with 5s of 2/2024 at 3.26%, 5s of 2027 at 3.31%, 5s of 2032 at 3.64%, 5s of 2037 at 4.10%, 5s of 2042 at 4.38% and 4.75s of 2048 at 4.70%, callable 2/15/2032.

J.P. Morgan Securities priced for the Indiana Finance Authority (Aa3/AA//) $150 million of green first lien wastewater utility revenue bonds, Series 2022B (CWA Authority Project) with 5s of 10/2023 at 3.24%m 5s of 2027 at 3.40%, 5s of 2032 at 3.73%, 5.25s of 2037 at 4.24%, 5.25s of 2042 at 4.56%, 5.25s of 2047 at 4.75% and 5.25s of 2052 at 4.85%, callable 10/1/2030.

In the competitive market, California (Aa2/AA-/AA/) sold $397.625 million of various purpose general obligation refunding bonds, Bid Group A, to BofA Securities, with 5s of 11/2023 at 3.14%, 5s of 2027 at 3.30% and 5s of 2028 at 3.35%, noncall.

The state also sold $312.235 million of various purpose general obligation refunding bonds, Bid Group B, to Wells Fargo, with 4s of 11/2029 at 3.39% and 5s of 2032 at 3.52%, noncall.

California sold $514.790 of various purpose general obligation refunding bonds, Bid Group C, to BofA Securities, with 5s of 1/2037 at 3.97% and 5s of 2042 at 4.21%, callable 11/1/2032, as well.

The New York City Transitional Finance Authority sold $212.590 million of taxable future tax-secured subordinate bonds, Fiscal 2023, Subseries D-2, to Morgan Stanley & Co., with 5s of 2027 at 4.85% and 5.35s of 2032 at par.

The authority also sold $137.410 million of taxable future tax-secured subordinate bonds, Fiscal 2023, Subseries D-3, to Wells Fargo, with all bonds pricing at par: 5.4s of 11/2034 and 5.65s of 2035, callable 11/1/2032.

The Spartanburg County School District No. 4, South Carolina, sold $100 million of general obligation bonds, Series 2022A, to Citigroup Global Markets, with 5s of 3/2025 at 3.25%, 5s of 2032 at 3.65%, 5s of 2037 at 4.05%, 5s of 2042 at 4.36%, 5s of 2047 at 4.55% and 5.25s of 2052 at 4.65%.

In the primary market, the tone has been relatively stable as deals are priced to sell with coupon structures not seen in a long time, Roffo said.

“Demand at the beginning of the month was primarily driven by cross-over buyers due to the cheapness of municipal bonds relative to Treasuries,” he said.

In addition, funds have been buying to restructure some of the lower-coupons purchased over the last few years causing spreads on the lower coupons to widen out, according to Roffo.

Secondary trading

Washington 5s of 2023 at 3.11%. NYC 5s of 2023 at 3.15% versus 3.18% Tuesday. California 5s of 2023 at 3.18% versus 2.83%-2.84% on 10/4 and 3.00% on 10/3. Georgia 5s of 2025 at 3.26% versus 3.15% Friday and 3.19% Thursday.

California 5s of 2027 at 3.30%. Triborough Bridge and Tunnel Authority 5s of 2028 at 3.44%. NYC 5s of 2029 at 3.49%. NYC TFA 5s of 2030 at 3.57% versus 3.19%-3.18% on 10/12 and 3.25% on 10/6. Maryland 5s of 2034 at 3.64%.

City and County of Denver, Colorado, 5s of 2037 at 3.88%. Greensboro, North Carolina, 5s of 2038 at 3.85% versus 3.89%-3.87% original on Tuesday. Connecticut special tax 5s of 2041 at 4.39% versus 4.20% Monday and 4.12% original.

Ohio waters 5s of 2046 at 4.35%-4.25%. NYC TFA 5s of 2047 at 5.04%-5.02% versus 4.76%-4.73% on 10/18. Northwest ISD, Texas, 5s of 2048 at 4.63%-4.57%. Virginia Public School Authority 5s of 2047 at 4.42%-4.30%. Austin, Texas, 5s of 2047 at 4.43% versus 4.41%-4.40% Tuesday.

AAA scales

Refinitiv MMD’s scale was cut up to 12 basis points out long: the one-year at 3.14% (unch) and 3.18% (unch) in two years. The five-year at 3.24% (unch), the 10-year at 3.41% (unch) and the 30-year at 4.16% (+12).

The ICE AAA yield curve saw big cuts out long: 3.17% (-1) in 2023 and 3.22% (-1) in 2024. The five-year at 3.26% (-1), the 10-year was at 3.47% (-1) and the 30-year yield was at 4.27% (+20) at a 4 p.m. read.

The IHS Markit municipal curve was cut two to 12 basis points: 3.16% (+2) in 2023 and 3.20% (+2) in 2024. The five-year was at 3.29% (+2), the 10-year was at 3.43% (+2) and the 30-year yield was at 4.15% (+12) at a 4 p.m. read.

Bloomberg BVAL was cut up to seven basis points out long: 3.11% (unch) in 2023 and 3.18% (unch) in 2024. The five-year at 3.24% (unch), the 10-year at 3.39% (unch) and the 30-year at 4.12% (+7) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.429% (-5), the three-year was at 4.401% (-6), the five-year at 4.203% (-5), the seven-year 4.117% (-6), the 10-year yielding 4.021% (-8), the 20-year at 4.382% (-10) and the 30-year Treasury was yielding 4.160% (-9) just before the close.

Primary to come:

The Triborough Bridge and Tunnel Authority is set to price Thursday $690.845 million of climate-certified payroll mobility tax senior lien green bonds, Series 2022E, consisting of $186.515 million of Series E-1, $99.560 million of Series E-2a and $404.770 million of Series E-2b. J.P. Morgan Securities.

The California Statewide Communities Development Authority is set to price $378.860 million of bonds (Enloe Medical Center), consisting of $208.955 million (/BBB-//), Series 2022A, serials 2024-2032, terms 2037, 2042, 2047, 2052 and 2057 and $169.865 million (/AA//), Series 2022B, term 2047, insured by Assured Guaranty Municipal Corp. KeyBanc Capital Markets.

The Michigan State Housing Development Authority is set to price Thursday $268.190 million of non-AMT social single-family mortgage revenue bonds, 2022 Series D. Barclays Capital.

Palomar Health, California, is set to price Thursday $215 million of tax-exempt certificates of participation, Series 2022A. Citigroup Global Markets.

Pinal County, Arizona, (/AA-/AA/) is set Thursday $109.625 million of pledged revenue obligations, Second Taxable Series 2022. Stifel, Nicolaus & Co.