Scale of California’s two state university systems felt in bond market

With a combined enrollment that is higher than the population of three U.S. states, California’s two massive state university systems, California State University and the University of California, have been major players on the bond market as they tend to their massive capital demands.

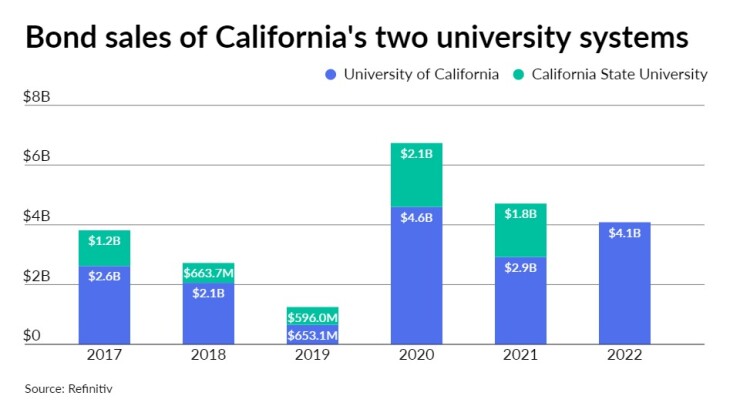

Between the two of them, they have issued more than $23 billion of debt since 2017, according to Refinitiv data.

Highlights of the capital projects funded by UC debt include seismic improvements to hospital buildings, while Cal State has issued bonds pay for construction to support science, technology, engineering, and math education and research.

Both are also funding building maintenance and renovations across their combined 33 campuses.

The university systems have both issued forward refundings as well to capitalize on low interest rates in a trend that developed after the 2017 federal tax bill eliminated advance refundings as an option.

“We have not issued, nor do we have any plans to issue debt this year,” said Robert Eaton, CSU’s assistant vice chancellor for financing, treasury, & risk management. The CSU trustees have sold $6.4 billion of debt since 2017 for the 23-campus system, which reported a fall 2021 enrollment of 477,466.

CSU had record debt sales in 2020, issuing $1.3 billion in bonds, and $1.9 billion in bonds in 2021, Eaton said.

“Our recent issuances were focused in 2019, 2020, and 2021,” Eaton said. “The new money was largely to support its academic and infrastructure program. Those are projects that don’t generate their own revenues.”

The bond issuance grew out of capital projects programs created in 2018-2019, Eaton said.

The CSU trustees approved $2.1 billion in authorization, and $2 billion in debt was issued for those programs. That money has helped fund projects across the 23 campuses, including seismic improvements for safety, and primarily academic building, some of which was construction to support STEM and research programs, he said.

The UC system has sold more than $16.9 billion of bonds since 2017, according to Refinitiv, and has kept the pace going into 2022.

In fiscal 2020-2021, the UC system, according to its most recent published annual financial report, sold more than $5.1 billion of revenue bonds, not counting a $411 forward delivery refunding delivered in fiscal 2022. The net increase of revenue bond debt for fiscal 2021 was $4.3 billion, according to the report.

“The University of California’s debt policy continues to guide its debt issuance, ensuring UC balances supporting its mission with maintaining its financial health,” said Stett Holbrook, senior communications strategist in the UC Office of the President.

The UC system has made significant forward delivery deals, working around the 2017 federal ban on tax-exempt advance refundings of bonds that haven’t reached call dates.

In August, for example, it priced a $1.09 billion deal that included a $318 million forward delivery component, scheduled to close in February 2023. Its 2032 maturity priced to yield 2.9%; less than two months later the Refinitiv MMD and IHS Markit triple-A 10-year benchmarks are at 3.16% as of Wednesday.

The UC system operates 10 campuses, five hospital systems and three national labs, and reported fall 2021 enrollment of 294,662.

The CSU and UC systems aren’t competitors, said Michael Osborn, a vice president and senior credit officer with Moody’s Investors Service.

The CSU system’s primary mission is “to serve Californians — more than 90% of its students come from California,” Osborn said.

“The UC system has a business, research mission, and a healthcare component. UC has more students from around the country and internationally; it is more diverse geographically than the Cal State system,” he said.

“CSU operates from a position of strength, it’s well-priced, and adds significant value to graduates,” Osborn said. CSU students “graduate with little to no debt, and the university system has a track record of providing graduates with a good social mobility trajectory.”

Given their size and management both were able to ride out COVID-19 fairly well.

The Moody’s ratings stayed the same, but UC’s outlook was revised to stable from positive in March, while CSU retained a stable outlook, Osborn said.

UC has ratings of Aa2 from Moody’s, AA from S&P Global Ratings and AA from Fitch.

CSU has Aa2 ratings from Moody’s and AA-minus ratings from S&P, which assigns a stable outlook.

Moody’s analysts noted leverage compared to its double-A rated university peers as a concern for CSU, but that includes its total debt; not just bond debt but also pension liabilities, Osborn said.

With total debt, its debt to spendable cash and investments ratio is 0.9 in audited year 2020, compared to the median of 1.5 for other similarly rated universities, Osborn said, noting that given Moody’s June analysis looked at 2020, the figures are somewhat dated.

But if Moody’s measures against cash flow, CSU’s debt relative to cash flow is more in line with its peers, he said.

“In our credit opinions, in the past, we have been quick to give praise to the fact the CSU system manages debt well,” Osborn said. “They have a robust capital planning process. Every project is vetted thoroughly. The university is not taking on more than it can chew.”

The UC system faces a significant challenge in getting its hospital buildings to meet California earthquake safety seismic mandates by the state’s 2030 deadline, Osborn said. The system has six medical schools, some with multiple hospitals.

“I can’t speak to where they are on their plan,” Osborn said. “They do publish a very detailed capital plan that is updated every year. Within that plan, you get a good sense of what their needs are across the system, one of those needs being seismic.”

As the system expands and modernizes it also addresses earthquake risks, he said.

“The UC system have been good stewards of their capital program,” Osborn said. “As I mentioned with Cal State, UC also has a very well managed capital plan. Debt issuance has been well paced, and we expect it be well paced and manageable going forward.”

In terms of the volume of debt, Osborn pointed to the size of the system.

“Each campus has its own capital plan, then multiply that by how many campuses each system has. It adds up to be significant capital plans,” Osborn said.

“The leverage profile of UC is manageable,” Osborn said. “It’s a well-managed capital program, in which each project is evaluated on its own merits.”

A ratings challenge for both systems is that they have significant pension liabilities, he said.

Total adjusted debt for UC by Moody’s calculations is more than $100 billion, which is the largest portfolio of debt from one entity that Moody’s tracks, he said. The direct bond debt is $27.8 billion by Moody’s calculation.

“They also have significant pension liabilities,” Osborn said. “But there are plans to address rising pension liability and the capital plan is well managed.”

The universities have both benefited from federal COVID-19 relief funds, and additional state funding in the fiscal year 2022-23 budget that saw a surplus of $97 billion.

CSU received a total increase of $365 million, including $221 million in unallocated funding and $81 million for enrollment growth, and $1.1 billion in one-time funding, according to a university press release that came after the budget was signed by the governor on July 1.

“The California State University is grateful for the significant investment in the CSU,” CSU Interim Chancellor Jolene Koester said in a statement. “Receiving ongoing funding totaling $365 million and one-time funding totaling $1.1 billion in the state budget agreement will enable us to address some mission-critical priorities, including increasing compensation for our valued employees and paying mandatory costs.”

Koester said the university will require a significant investment in staffing looking forward.

“Compensation and critical deferred maintenance and facility needs still remain,” Koester said. “Considering the state’s unprecedented funding surplus, it is disappointing that additional support to address these important priorities was not allocated.”

She did laud the governor’s plans in his multi-year compact pledge to “propose predictable and reliable levels of funding in the future, as well as protection against economic uncertainty.”