Munis improve to start week; increased supply to test market

Munis were slightly better to kick off the week, while U.S. Treasuries were firmer 10 years and in and equities rallied.

Municipal triple-A yields fell one to three basis points Monday while UST saw the 10- and 30-year end the session just above 4%.

“Municipal bond yields decoupled from the Treasury market last week, ending basically unchanged,” said Nuveen strategists Anders S. Persson and John V. Miller. Ratios on Monday showed further richness for munis.

Muni-UST ratios saw the three-year on Monday at 67%, the five-year was at 70%, the 10-year at 78% and the 30-year at 93%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the three at 66%, the five at 70%, the 10 at 80% and the 30 at 93% at a 4 p.m. read.

Last week’s calendar was very light due to the holiday-shortened week and the release of the consumer price index report on Thursday, noted Jason Wong, vice president of municipals at AmeriVet Securities. This week, volume rebounds eightfold with a new-issue calendar of $8.5 billion, including several billion-dollar deals.

While there was only four days of trading last week, he said there was about $43 billion in secondary trading as “volatility continues to hit the markets as accounts are still worried about high inflation, a possible recession and the potential of more rate hikes.”

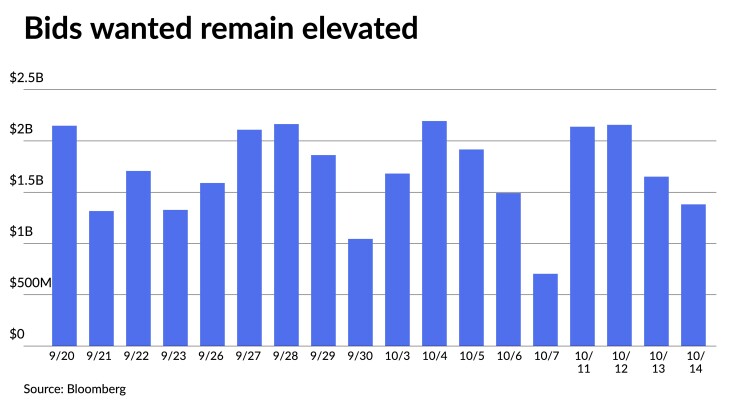

Wong said clients’ bids wanteds continue to be at “elevated levels with about $7.33 billion in total par amounts,” per Bloomberg data.

“Muni yields for the week rose slightly with the 10-year notes rising by just 1.6 basis points to 3.16% as munis sold off due to the higher-than-expected inflation numbers on Thursday,” he said. But despite munis finishing the week weaker, they outperformed USTs as “Treasury yields increased dramatically because of the CPI number.”

With the release of the CPI figures, inflation continues to be at elevated levels, resulting in triple-A yield curves being cut, with larger losses on the short end, while USTs saw yields rise nine 18 basis points five years and in, he said.

“Although we did not see the sharp increases in yields as we saw in Treasuries, keep in mind that munis usually lag Treasuries as we are seeing the muni curve continue to flatten even more,” Wong said. “Since the beginning of the third quarter, we have seen the short end yield rise by about 150 basis points, while the 10-year portion only increasing by roughly 70 basis points, and the long by just 65 basis points.”

Fed rate increases should continue, at least for now, Nuveen said. The 10-year UST reached 4% last week (and held there on Monday), which remains inverted relative to short-term yields. This suggests, they said, that investors believe the Fed will keep raising short-term rates.

“Many expect the Fed will be successful by the second quarter of 2023 when long-term rates should rally,” they said.

But the muni market continues to be an area of opportunity, said Cooper Howard, fixed income strategist focused on munis at Charles Schwab.

“Yields have risen significantly and credit risk remains low,” he said.

“We think the bulk of the move up in yields is behind us so we favor extending duration and focusing on higher-rated issuers,” Howard noted. “Relative yields have declined recently but and are more attractive the further out the yield curve you move.”

However, fund flows continue to remain negative pressuring spreads, he said.

While yields are attractive, he said that “investors continue to pull money out of muni mutual funds and ETFs at a record pace,” putting “upward pressure on credit spreads even though credit risks aren’t on the rise.”

Muni bonds, though, remain resilient.

“While mutual funds have seen redemptions, individual investors have supported the market with heavy interest, as they can buy bonds with a tax-exempt 4% yield,” Nuveen strategists said. “Institutional investors also continue to rework their portfolios.”

They believe there will be continued volatility through the rest of the year but expect a better year in 2023.

Secondary trading

Michigan 5s of 2023 at 2.92%-2.91%. Georgia 5s of 2024 at 2.91% versus 2.96% Friday and 3.03%-3.00% original on 10/7. NYC 5s of 2024 at 2.99% versus 3.01%-2.92% Friday and 3.07%-3.02% Thursday. California 5s of 2024 at 2.90%-2.92% versus 2.95% Tuesday.

LA DWP 5s of 2027 at 2.96%. Washington 5s of 2029 at 3.16%-3.15%. Georgia 5s of 2029 at 3.03% versus 3.02% Thursday.

NYC TFA 5s of 2031 at 3.29%-3.34% versus 3.32% Friday. University of California 5s of 2032 at 3.10%-3.08% versus 3.11% Tuesday. Maryland 5s of 2033 at 3.27%-3.26% versus 3.29%-3.28% Thursday.

DC 5s of 2042 at 3.91%. Washington 5s of 2046 at 4.07% versus 4.12%-4.11% Thursday and 4.10% on 10/7.

San Diego County Water Authority 5s of 2052 at 4.08%-4.05%. California 5s of 2052 at 4.17%.

AAA scales

Refinitiv MMD’s scale was bumped two basis points: the one-year at 2.91% (-2) and 2.95% (-2) in two years. The five-year at 2.98% (-2), the 10-year at 3.13% (-2) and the 30-year at 3.74% (-2).

The ICE AAA yield curve was bumped one to three basis points: 2.95% (-1) in 2023 and 2.98% (-1) in 2024. The five-year at 3.02% (-1), the 10-year was at 3.21% (-2) and the 30-year yield was at 3.76% (-2) at a 4 p.m. read.

The IHS Markit municipal curve bumped one basis point: 2.91% (-1) in 2023 and 2.93% (-1) in 2024. The five-year was at 3.00% (unch), the 10-year was at 3.13% (-1) and the 30-year yield was at 3.73% (-1) at a 4 p.m. read.

Bloomberg BVAL was bumped one to two basis points: 2.97% (unch) in 2023 and 2.99% (-1) in 2024. The five-year at 3.03% (-2), the 10-year at 3.15% (-1) and the 30-year at 3.79% (-1) at 4 p.m.

Treasuries were firmer 10 years and in.

The two-year UST was yielding 4.458% (-4), the three-year was at 4.454% (-5), the five-year at 4.246% (-2), the seven-year 4.150% (-2), the 10-year yielding 4.020% (flat), the 20-year at 4.302% (flat) and the 30-year Treasury was yielding 4.023% (+2) at the close.

Primary to come:

Connecticut (Aa3/AA-/AA-/AA+) is set to price Tuesday $1.143 billion, consisting of $830 million of special tax obligation bonds, transportation infrastructure purposes Series A, serials 2023-2043 and $312.730 million of special tax obligation refunding bonds, transportation infrastructure purposes, Series B, serials 2024-2033. Siebert Williams Shank & Co.

Massachusetts (Aa1/AA/AA+/) is set to price Wednesday $1.105 billion of general obligation bonds consolidated loan of 2022, Series C, and general obligation refunding bonds, Series A, consisting of $1 billion of Series 1 and $104.770 million of Series 2. Morgan Stanley & Co.

CommonSpirit Health, Colorado, (Baa1/A-/A-/) is set to price Tuesday $1 billion of taxable corporate CUSIPs. J.P. Morgan Securities.

The nonprofit hospital chain also is set to price Tuesday $500 million of the Colorado Health Facilities Authority revenue bonds, consisting of $250 million of Series A, $125 million of Series B-1 and $125 million of Series B-2. J.P. Morgan Securities

Hawaii (Aa2/AA+//) is set to price Wednesday $800 million of taxable general obligation bonds, Series GK. Morgan Stanley & Co.

The New Jersey Economic Development Authority (A3/BBB+/A-/) is set to price Wednesday $583.245 million of Portal North Bridge Project NJ Transit transportation project bonds, Series A, serials 2023-2042, terms 2047 and 2052. Barclays Capital.

The Southeastern Pennsylvania Transportation Authority (Aa3//AA/AA/) is set to price Tuesday $511.965 million of Asset Improvement Program revenue bonds, serials 2024-2042, terms 2047 and 2052. Citigroup Global Markets.

Wisconsin (Aa1/AA+//AAA/) is set to price Wednesday $249.240 million of general obligation refunding bonds, Series 4. Jefferies.

The Liberty Hill Independent School District, Texas, (Aaa///) is set to price Tuesday $196.025 million of unlimited tax school building and refunding bonds, Series A. Piper Sandler & Co.

The New Braunfels Independent School District, Texas, is set to price Thursday $194.595 million of unlimited tax school building and refunding bonds, Series B. Piper Sandler & Co.

The Ohio Housing Finance Agency (Aaa///) is set to price Thursday $149.995 million of non-AMT social Mortgage-Backed Securities Program residential mortgage revenue bonds, Series C, serials 2024-2034, terms 2037, 2042, 2047, 2053 and 2054. Citigroup Global Markets.

The Rhode Island Housing And Mortgage Finance Corporation (Aa1/AA+//) is set to price Thursday $128.460 million of homeownership opportunity bonds, consisting of $113.460 million of non-AMT social bonds, Series 78-A and $15 million of taxable bonds, Series 78-T. J.P. Morgan Securities.

New Orleans (A2/A+/A/) is set to price Wednesday $122.695 million of general obligation refunding bonds. J.P. Morgan Securities LLC, New York

The Connecticut Housing Finance Authority (Aaa/AAA//) is set to price Wednesday $118.135 million of social Housing Mortgage Finance Program bonds, Series E, Subseries E-1, serials 2023-2034, terms 2037, 2042, 2045 and 2052. Citigroup Global Markets.

The Indiana Finance Authority (Aaa/AAA/AAA/) is set to price Tuesday $105 million of green State Revolving Fund Program bonds, Series D. Morgan Stanley & Co.

The Municipality of Anchorage, Alaska, (/AA//) is set to price Thursday $100.775 million of solid waste services revenue refunding bonds, Series A. J.P. Morgan Securities.

The Miracosta Community College District, California, (Aaa/AAA//) is set to price Wednesday $100 million of Election of 2016 general obligation bonds, Series C. Piper Sandler & Co.

The Mountain View Whisman School District, California, (Aaa/AAA//) is set to price next week Election of 2020 general obligation bonds, Series B. RBC Capital Markets.

Competitive:

St. Johns County, Florida, (Aa2/AAA//) is set to sell $120.945 million of water and sewer revenue bonds at 10:30 a.m. eastern Tuesday.

Rhode Island (Aa2/AA/AA/) is set to sell $162.450 million of general obligation bonds consolidated capital development loan of 2022, Series A, at 10:15 a.m. Tuesday, and $60.300 million of taxable general obligation bonds consolidated capital development loan of 2022, Series A, at 10:45 a.m. Tuesday.

The Virginia Public School Authority (Aa1/AA+/AA+/) is set to sell $103.660 million of 1997 Resolution school financing bonds at 10:30 a.m. Tuesday.