Stronger tone continues while ICI reports $5.4B of outflows

Municipals were little changed to stronger on the short end as U.S. Treasuries saw losses mount and equities closed out the session in the red.

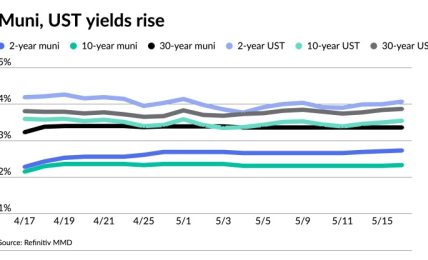

Triple-A yields were mixed to firmer on the short end, depending on the yield curve, while UST ended with the largest losses in the belly of the curve.

Municipal to UST ratios fell on the day’s moves. The three-year on Wednesday was at 72%, the five-year was at 76%, the 10-year at 84% and the 30-year at 99%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the three at 73%, the five at 78%, the 10 at 90% and the 30 at 101% at a 4 p.m. read.

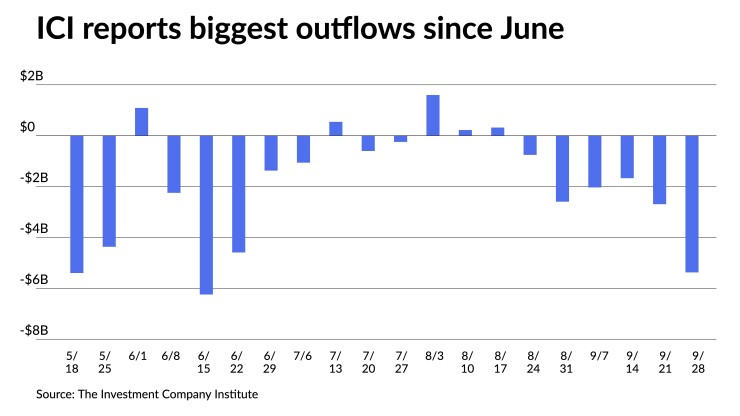

The Investment Company Institute reported the largest outflows from municipal bond mutual funds since mid-June in the latest week and exchange-traded funds continued their outflow cycle.

ICI reported $5.374 billion of outflows for the week ending Sept. 28 after $2.693 billion of outflows the previous week.

ETFs saw outflows of $292 million after $492 million of outflows the week prior, per ICI data.

With ongoing UST volatility and global macroeconomic headline risks, munis are experiencing a tug of war, said Manish Jain, Fixed Income Portfolio Manager at Zacks Investment Management.

“You’re still seeing liquidations coming in from investors who are in bond funds,” he said. “Also, they’re going to be getting their monthly statements, quarterly statements and see their performance numbers year-to-date are down. And we’ve been steadily seeing sales coming in from that side.”

This has put some pressure on the market.

“Pretty much every single week, we have seen $1 billion here, $2 billion here, $3 billion [last] week, that we’ve been told, retail investors getting out or so,” he said. “I wish I could say it was a stable market, but it’s definitely not, a lot of crosscurrents going on in the market right now.”

“Investors have been selling, and this is despite munis doing better than corporates and Treasuries as well,” he said. “But investors who had gotten so used to positive returns on a year-by-year, when the rates were coming down, all of a sudden, now they’re looking at 10% to 15% declines. And that’s a little bit of a shock to them.”

All eyes are turning to this week’s jobs report.

“The labor market has remained resilient in the face of high inflation, rate hikes, and slowing economic growth,” said Cooper Howard, fixed income strategist focused on munis at Charles Schwab.

“If payroll growth continues to be strong, the Fed will need to follow through on its aggressive pace of rate hikes. Average hourly earnings will be key — if wage growth remains strong, inflation should remain elevated.”

Howard says Schwab’s guidance for their clients is to continue to gradually extend duration of their bond holdings.

“With yields at post-financial crisis highs, we suggest investors lock in yields with certainty rather than waiting for the Fed to stop hiking rates,” he said.

Secondary trading

Mecklenburg County, Maryland, 5s of 2023 at 2.94%-2.91%. That issue priced on August 16 100 basis points lower at 1.90%.

Howard County, Maryland, 5s of 2023 at 2.95%. District of Columbia 5s of 2024 at 3.03%-3.02%. Loudoun County, Virginia, 5s of 2024 at 3.07%-3.06%. Wake County, North Carolina, 5s of 2025 at 3.07%-3.05%.

Prince George’s County, Maryland, 5s of 2027 at 3.11%. Texas waters 5s of 2027 at 3.12%. California 5s of 2027 at 2.98% versus 3.09% Tuesday. Maryland 5s of 2027 at 3.07% versus 3.11%-3.10% Tuesday.

New York City TFA 5s of 2028 at 3.17% versus 3.19% Tuesday. California 5s of 2029 at 3.17%-3.13% and 5s of 2030 at 3.19%-3.16%.

New York Dorm PITs 5s of 2041 at 4.21%-4.20% versus 4.43% Thursday. New York UDC PITs 5s of 2046 at 4.41%-4.39% versus the same as Tuesday, 4.54%-4.53% Monday and 4.61% original.

LA Department of Water and Power 5s of 2052 at 4.10%. New York City waters 5s of 2052 at 4.41%.

AAA scales

Refinitiv MMD’s scale saw small bumps on the short end: the one-year at 2.95% (-4) and 2.97% (-4) in two years. The five-year at 3.02% (-2), the 10-year at 3.18% (unch) and the 30-year at 3.74% (unch).

The ICE AAA yield curve was little changed: 2.98% (unch) in 2023 and 3.02% (unch) in 2024. The five-year at 3.05% (unch), the 10-year was at 3.23% (unch) and the 30-year yield was at 3.76% (+1) at a 4 p.m. read.

The IHS Markit municipal curve was bumped on the short end: 2.95% (-4) in 2023 and 2.97% (-4) in 2024. The five-year was at 3.06% (unch), the 10-year was at 3.16% (unch) and the 30-year yield was at 3.75% (unch) at a 4 p.m. read.

Bloomberg BVAL was mixed: 2.94% (-1) in 2023 and 2.97% (-1) in 2024. The five-year at 3.02% (unch), the 10-year at 3.14% (+1) and the 30-year at 3.77% (unch) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.146% (+4), the three-year was at 4.161% (+6), the five-year at 3.956% (+10), the seven-year 3.866% (+12), the 10-year yielding 3.745% (+11), the 20-year at 4.044 (+6) and the 30-year Treasury was yielding 3.751% (+5) at the close.

Primary to come:

Austin, Texas, (Aa2/AA/AA-/) is set to price Thursday $299.500 million of water and wastewater system revenue refunding bonds, Series 2022. Jefferies.

The city also is set to price $200.010 million of forward-delivery water and wastewater system revenue refunding bonds, Series 2023. Jefferies.