Positive momentum for munis to start Q4

Municipals made gains Monday, underperforming a stronger U.S. Treasury market, but taking advantage of the positive tone of all markets as equities also rallied to open the fourth quarter.

Triple-A benchmarks were bumped one to six basis points, depending on the scale, while U.S. Treasury yields fell 16 to 19 basis points 10 years and in with gains of eight to nine out long.

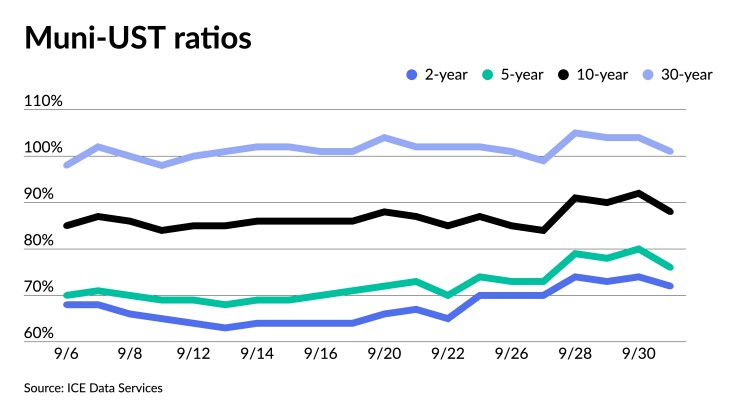

Municipal to UST ratios fell slightly. The three-year on Monday was at 75%, the five-year was at 79%, the 10-year at 88% and the 30-year at 103%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the three at 72%, the five at 76%, the 10 at 88% and the 30 at 101% at a 4 p.m. read.

While munis opened the month stronger, September leaves behind 3.84% losses — the single largest monthly loss since September 2008 — bringing year-to-date losses to 12.13%, per the Bloomberg Municipal Index. High-yield lost 6.16% in September and is 16.03% in the red in 2022 while taxable munis lost 5.12% in the month and 15.58% year-to-date.

“September has been an excruciatingly painful month for municipal bonds” and they “are still on pace to have their worst year of performance since the 1980s when records were kept,” said Jason Wong, vice president of municipals at AmeriVet Securities.

This September was “the worst-performing month since September of 2008 as the continuation of aggressive interest rate hikes by the Fed have battered fixed income markets,” he noted.

He noted the long end is most concerning “as losses have amounted to almost 20% while the short end has lost only 2.34%.” But even though losses are “greater as you go further out into the curve, investors should start to look further out into the curve as ratios are starting to turn in favor of munis,” Wong noted.

Ratios for five- to 10-year munis have risen over six percentage points in the past week while two- to three-year munis have only risen by four percentage points, he said.

“Secondary trading continues to be very volatile as rising interest rates have caused the markets to go into a frenzy,” Wong said.

Last week, secondary trading for the week totaled to around $53.5 billion, with 52% of the trades being dealers selling to clients.

Client’s bids-wanted was also high for the week with about $8.77 billion, up from $8.18 billion the week prior.

“Clients’ bids-wanted continues to be high as many investors continue to pull money out of mutual funds due to rising interest rates from the Fed’s policy of raising interest rates to combat high inflation,” Wong said.

Outflows intensified once more last week as investors pulled about $3.6 billion out of municipal bond mutual funds last week versus $2 billion of outflows from the prior week according to Refinitiv Lipper, marking the eighth straight weeks of outflows.

“Muni funds continue to feel the pain as rising interest rates has many investors continuing to wait on the sidelines until the volatility subsides,” Wong said. “We should outflows continue until we start to see the volatility in the markets to subside.”

But while investors are fleeing muni mutual funds, CreditSights strategists Pat Luby and John Ceffalio believe they will return.

“Through the first eight months of the year, total gross purchases of municipal bond mutual funds exceed the average full-year total for the 10-year span from 2012 to 2021,” they said.

Municipal bond mutual fund buyers have purchased $271 billion of shares, as of Aug. 31, compared to the recent annual average of $216 billion. Full-year gross purchases were $308 billion and $293 billion in 2020 and 2021, respectively, they said.

Year-to-date net flows are down “so much because of the sharp increase in mutual fund redemptions,” which total $361 billion through the end of August. “That is more than the full-year redemptions since at least 2009 and is almost double the 2012 to 2021 average of the $185 billion,” they said.

“This year’s higher yields appear to be attracting income-oriented investors while they are also repelling other investors with existing positions in the mutual funds,” CreditSights strategists noted.

Secondary trading

California 5s of 2023 at 3.08%-3.03%. The Board of Regents of the University of Texas System 5s of 2024 at 3.12%. Georgia 4s of 2025 at 3.08% versus 3.20%-3.12% Friday. Maryland 5s of 2027 at 3.15% versus 3.18% Friday.

Triborough Bridge and Tunnel Authority 5s of 2030 at 3.39%-3.35% versus 3.48% Wednesday. Maryland 5s of 2033 at 3.40% versus 3.46% Friday. NYC TFA 5s of 2035 at 3.93% versus 3.97% Friday.

NYC Municipal Water Finance Authority 5s of 2045 at 4.42%-4.44% versus 4.40%-4.43% on 9/26. Washington 5s of 2045 at 4.14% versus 4.06% on 9/22 and 4.02%-4.03% on 9/21. Texas Water Development Board 5s of 2047 at 4.30%-4.26% versus 4.45%-4.36% original on Thursday.

AAA scales

Refinitiv MMD’s scale was bumped three to six basis points: the one-year at 3.03% (-3, no Oct. roll) and 3.06% (-3, no Oct. roll) in two years. The five-year at 3.09% (-3, no Oct. roll), the 10-year at 3.24% (-6, no Oct. roll) and the 30-year at 3.84% (-6).

The ICE AAA yield curve was bumped two to four basis points: 3.05% (-2) in 2023 and 3.09% (-2) in 2024. The five-year at 3.12% (-4), the 10-year was at 3.32% (-4) and the 30-year yield was at 3.85% (-3) at a 3:30 p.m. read.

The IHS Markit municipal curve was bumped one to six basis points: 3.03% (-1) in 2023 and 3.07% (-3) in 2024. The five-year was at 3.13% (-3), the 10-year was at 3.26% (-6) and the 30-year yield was at 3.85% (-6) at a 4 p.m. read.

Bloomberg BVAL was bumped three to four basis points: 2.99% (-3) in 2023 and 3.01% (-4) in 2024. The five-year at 3.07% (-3), the 10-year at 3.20% (-4) and the 30-year at 3.84% (-4) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.123% (-16), the three-year was at 4.128% (-16), the five-year at 3.901% (-19), the seven-year 3.789% (-20), the 10-year yielding 3.661% (-17), the 20-year at 4.000 (-9) and the 30-year Treasury was yielding 3.710% (-8) near the close.

Primary to come:

New York City (Aa2/AA/AA-/AA+/) is set to price Tuesday $950 million of tax-exempt general obligation bonds, Fiscal 2023 Series B, Subseries B-1, serials 2024-2047. Citigroup Global Markets.

The city also is set to price Tuesday $400 million of taxable general obligation social bonds, Fiscal 2023 Series B, Subseries B-2, term 2052. Citigroup Global Markets.

The Spring Branch Independent School District, Texas, (Aaa/AAA//) is set to price Tuesday $308.430 million of unlimited tax schoolhouse bonds, Series 2022, insured by the Permanent School Fund Guarantee Program. Jefferies.

Austin, Texas, (Aa2/AA/AA-/) is set to price Thursday $299.500 million of water and wastewater system revenue refunding bonds, Series 2022. Jefferies.

The city also is set to price $200.010 million of forward-delivery water and wastewater system revenue refunding bonds, Series 2023. Jefferies.

The Sabine-Neches Navigation District, Texas, (Aa2///) is set to price Tuesday $173.370 million of Sabine-Neches Waterway Project limited tax bonds, Series 2022, serials 2024-2042, terms 2047 and 2052. Jefferies.

California (Aa2/AA+/AA/) is set to price Wednesday $166.935 million of non-AMT veterans general obligation bonds, Series CU, serials 2023-2034, terms 2037, 2042, 2046 and 2052. Wells Fargo Bank.

Competitive:

The Bridge City Independent School District, Texas, is set to sell $72.400 million of unlimited tax Permanent School Fund Guarantee Program school building bonds, Series 2022, at 12 p.m. eastern Wednesday.